Grow up, pension, big and state. How to increase your pension?

When calculating the monthly payment, the entire amount of your pension is divided by the number of remaining months in the “survival” period. When you reach retirement age this period is 228 months. Therefore, the later you apply for your pension, the more you will receive each month. In addition, by continuing to work, you extend your work experience and accumulate points.

Secret 2. The funded part of the pension

Until the end of this year, citizens born in 1967 and younger can decide to receive the funded part of the pension in addition to the regular insurance one. You will be able to manage these funds now by investing them in non-state pension funds and management companies. They, in turn, will invest them and bring you profit. The main thing here is not to make a mistake in choosing the company to which you entrust your money.

There are few options for companies to whom to entrust your future pension.

It's either state management company - Vnesheconombank. Engaged in investing in government securities and bonds, also offers an expanded portfolio in which you can invest in deposits in credit institutions and bonds of constituent entities of the Russian Federation.

Or non-state pension fund (NPF). Invests in management companies of his choice. You cannot influence either their choice or quantity.

And finally, private management companies (MCs). They offer a choice of several investment portfolios with securities.

Secret 3. Endowment insurance

The essence of this system is that you pay constant premiums to the insurance company over several years. To these are added the investment income that the insurance company receives from using your money. The result is an amount that can either be received immediately upon reaching retirement age, or spread over time, ensuring a lifetime pension.

Secret 4. Security deposit

This is a type of bank deposit that also provides life insurance. The investor will deposit the amount for up to ten years and receive an income from it from 7 to 10.5% per year. However, remember that deposits are subject to inflation, and amounts greater than 700 thousand rubles are not insured by banks.

Secret 5. Pension contribution

Today, many banks offer special deposits for pensioners in different currencies. They differ from ordinary ones by a higher interest rate - from 3 to 11% per annum.

Even if you are still far from retirement age, it is worth taking care of future payments. To provide yourself with a pension, pay attention to the size of your salary and length of service. They directly influence the formation of the amount of future payments. Also, give preference to white salary. It ensures that your employer pays mandatory contributions. pension insurance.

For each year of work you receive points, which are then added up and converted into rubles. Remember that you must meet certain requirements to receive your pension. For example, today you need to work for at least 6 years and earn at least 30 pension points.

Anastasia Mironova

One day I started talking about retirement with a dentist and suggested that we think about it and save up for it. A man, about 35-38 years old, does dentures, and I have a couple of his “works” in my mouth. I have no complaints about his work

But when I talked to him about his pension, he told me directly and honestly that he had not thought about it yet. Apparently, his stereotypes of the past are so strong, when our “kind” state will give him a pension after the end of the “terms of squeezing out all the juices.” I could tell from his tone that he wasn't going to think about it any further. Now he is on a wave of success, his services will always be in demand in the future, and therefore he is not thinking about retirement. He doesn't think yet. One can only guess what motivates him in this “not thinking.” Probably, this is his demand and confidence that it will always be like this in the future. But now our life has become less predictable. No one can say that it will always be like this in the future, not a single person. And life changes, alas, not always for the better.

Here, a seemingly very prominent official recently left (or rather, he was “left”), and people began to discuss on the Internet why he left without a “golden parachute?” Yes, indeed, why? He also thought that a system in which he was not the last person and not a “cog”, and he was supported by the highest-ranking officials of the state, this system would forever protect him and his “pranks” would be looked at just as condescendingly, without “noticing” their. But “suddenly” everything changed, although everyone seemed to be waiting for it to finally be filmed. Even the deadlines for its removal were announced, but something changed, and it “flew” not so long ago. But it still flew off! “It’s good” that “some” of us are not shaken, giving them the opportunity to put their financial affairs in order and retire to other countries with this money. These people manage to hide their ends in the water. Examples are before everyone's eyes.

Why would this be a legitimate question...

But what should a mere mortal who was not born almost a “celestial being” do? In one of the books, I read the recommendations of one smart entrepreneur on how to create a decent pension for himself. What is a decent pension, you ask? I will answer, quoting that entrepreneur, that this is the pension that, once accumulated, “is a million dollars or so.” Enough for a comfortable old age? Who cares... But there are options, and I offer them for discussion. The main thing is to convey the essence to you...

And the point is this. I wrote in my previous opus about how our banking system is thriving. Is it possible to involve banks in the formation... of your pension? What should be done for this? And you need to do the following.

Need to whole year do the same thing: every day put aside one dollar or its ruble equivalent of 30 rubles. You can start even tomorrow, even on January 1st. And just like that, by putting aside one dollar at a time, by December 31st we will already have 365 dollars. If you multiply by some thirty rubles, which are usually used in calculations, you get 10,950 rubles or 912.5 rubles per month. It's real? Yes, rather, yes. This amount of 10,950 rubles must be available by January 1 of the next year. Holding this money under your armpit and continuously saving for the next 10 days (days until the first day of the bank's work after the New Year :-)) already in the new year, you need to run to the bank on its first working day, the 10th, say, January and, having opened an account there, put this money into a deposit account at a certain percentage, but what? The book I read indicated 20 percent, but I have never heard of any of our banks operating at such percentages. The real percentage is up to 12. Not enough? Yes, very much, but we’ll figure this out later and how to increase it. For simplicity of calculations, let’s take a very real percentage - 10. It’s these 10% that we’ll take for the mathematical model of our future pension. Yes, one more circumstance is needed - age, which should be such that you can do this for about 40 years, so that by retirement the number of years of accumulation will be maximum. Let's take 40 years for simplicity of calculations, but do not be upset if you missed this time and you are not 23 years old now - the end of your student life. Now we have all the indicated data to calculate the pension. Let's say, for simplicity, that we have saved up $365 and start on January 1, and not on the 10th, when the rest period for bankers and their employees ends. I repeat that instead of the first of January, the day can be any, even tomorrow, November 24, chosen to start accumulating. Let us still accept the first of January for simplicity and clarity of calculations.

So, on January 1, 2013, you open a bank account at 10% per annum, and a year later, on January 1, 2014, your bank should be ready to give you the entire accumulated amount - 365 + 36.5 dollars for “renting” your money. Hurray, the first step has been taken, the most important and significant! You have laid the most important stone in the foundation of your retirement. Then I'll tell you why. You came to the bank, but you are a smart person and will not take your money from the bank, but rather put in another 365 dollars or 10,950 rubles, which you have accumulated over the entire 2013.

In January 2015, your income will be $36.5 from the money deposited in 2014 (this is 10% plus some other amount). This amount will be 10% more than the sum of 365 and 36.5 or (365+36.5)x10%=$40.15. Thus, in 2 years you “grew” 36.5 and 40.15 dollars = 76.65 dollars. It is worth noting that the increase in the second year will be 40.15 dollars, and not 36.5, as it was in the first year, that is, the rule of compound interest - “interest on interest” - applies. This is the meaning of this system, that is, every subsequent year you grow an ever-increasing amount of money received from the very first deposit made, as we agreed, in 2013. But then in 2015 the second deposit also grew, but only by 10% and it will bring you its usual first 36.5 dollars. Once again, let’s calculate how many dollars our contributions or investments, as they are pathetically called, brought in: the very first contribution in 2 years brought 36.5 plus 40.15 dollars, but the second contribution also brought in an increase of 36.5 dollars over the year. In total, 2 times 36.5 plus 40.15 will give 113.15 dollars for the investment 2 times 365 or 730 dollars. This, of course, is a trifle, but this is what needs to be considered and seen here. The very first thing is that the first installment brought in not 36.5, but 40.15 dollars, and the second installment brought its 10% or 36.5 dollars, that is maximum amount The growth will always be given by the earliest contribution or contribution or the very first investment. And another thing worth considering here is that the second contribution exactly repeats the first contribution in terms of results, as if the first one was “moved” back a year and the results of its previous, second year were taken away, that is, these 40.15 dollars and then these contributions and their results would be completely equal. What follows from this? The fact that we can continue to build a mathematical model of our pension: having deposited our third 365 dollars in 2015, we will receive a year later in 2016 36.5 dollars from what was invested in 2015, plus 36.5 plus 40.15 from what was invested in 2014. But to determine how much we will get from the investment in 2013, we need to calculate it slowly. This contribution, the very first one, will bring us the maximum, as mentioned, that is, 36.5 plus 40.15 plus 10% of the amount of 36.5 dollars, 40.15 and 365 dollars, that is (36.5 + 40.15 + 365) x 10% = 44.17 dollars, that is, in the third year the first payment will bring 44.17 dollars, the second will bring 40.15 dollars, and the third will bring 36.5 dollars, and in total three payments will bring in at the end of the third year amounted to $120.82. Next year everything should be repeated: you make a contribution of 365 dollars and a year later you get the following picture: from the last contribution you receive 36.5 dollars, from the second to last 40.15, from the third from the end 44.17, and from the very first payment will be such (36.5 + 40.15 + 44.17 + 365) x 10% = 48.58 dollars, and in total we get an increase equal to 169.40 dollars. If the mechanism for creating a pension is clear, then you can make a calculation for 40 years or as many years as you plan to “grow” your pension. You need to understand the most important thing: the mechanism for calculating profit after the very first year from the very first installment and then from the second installment after it has been in the bank for one year. The very first profit is 365x10% = 36.5 dollars from the first payment, and in the second year the profit is considered to be 10% of the amount 365 + 36.5, that is, (365 + 36.5) x 10 = 40.15 dollars, that is, under the number from which 10% is taken, an ever-increasing amount comes: first only from 365 dollars, then from 365 dollars plus 10% of 365 = 36.5 dollars, then the amount from the flowing money and so on. And all subsequent calculations are similar to the previous ones without profit last year. The interest from this rate of 10% begins to further increase rapidly and the curve of the first payment itself goes up steeper and steeper. The growth curve from the second installment fits under it, and the curve of the third year of investment fits under it with an annual indent. By summing up the ordinates of these curves after 40 years or more, you will get very happy results. Try this by taking a calculator and plotting savings graphs for each year and summing up the graphs to get the result. It's not that long

The question arises, who is stopping you from doing the same operation with investments 2 times a year or three or four times? As they say, who has what opportunities... But for this you need to leave accordingly every day not thirty, but sixty, ninety, one hundred and twenty rubles. Or you can save 100 rubles every day... This is where you get “at 20%”, “at 30%”, “at 40%”. Calculate your own results over 40 years of investment. There is no reason for pessimism! Old age is completely guaranteed for you! And perhaps not only you! Should we expect any concessions from our state? Under the “damned” Soviet system, many received their 134 rubles as a monthly pension, and this was not enough for a comfortable life. Well, wait, wait, if you hope... You need, I think, to make a very good end to your life in retirement, yourself. After all, now there is so much talk about pension reform and about the accumulation of this very pension. And where are they? It is known where. And I propose to do it this way. I repeat that this is not my invention, but that of this smart entrepreneur, whose book I read several times and, unlike you, was not too lazy to do the calculations. As I said here, you can't argue with math. And this is what “grows” out of $365 over 40 years of savings: do the math. The savings for 39 years are added to them, then for 38, 37 and so on. And the last savings will be for one year in the form of 36.5 dollars, which you made, if you do this, in the 39th year of savings. By adding up all the ordinates of this “branchy” graph, you will be convinced that you can accumulate a huge amount, giving you the opportunity to live comfortably at the end of your life. What if you do this procedure 2 times a year?

5.12.12. Knowing and being 1000% sure that not one of you reading this will take a calculator and calculate the results, “Your humble servant” took the risk of doing all these calculations, and this is what happened. Over 40 years of such “savings activity” it would be possible to accumulate $132,911.96. Of these, $14,600 is the accumulation of deposits of $365, and the remaining $118,311.96 will be given to us by the bank for the 40-year use of our accumulated $14,600. At an exchange rate of 30 rubles for 1 dollar, this would be 3,987,358.8 rubles, and if you spend 25,000 rubles a month, which most pensioners cannot do, you can live on this for 3,987,358.8: 25,000 = 159.5 months or 13.3 years. With certain savings, this period can be longer. Now, if you continue to accumulate according to the same system for another 8 years, then during this time you can receive another certain amount, and together with the previously accumulated amount it will be 340,719.74 of the settlement dollars I received, multiplying which by 30 we get 10,221,592.2 rubles, which is Spending 25,000 a month will be enough for almost 409 months or 34 years of life. So there is something in this mathematical model, in my opinion, that deserves attention. The entrepreneur who wrote the book promised a million dollars at 20% per annum given by the bank, but, I repeat, we must be realistic and look at the figures that are available to us. That’s why I took the risk of doing calculations and recommendations on how to save myself a decent pension. Think about how you will live in the future. And how will you live on what the state will give you when you retire? The state is for me labor activity from 14 years old to 60 years old did not hesitate to write to me pension certificate: two thousand five hundred fifty-seven rubles 26 kopecks. For life. Would you be happy with this option? Now, of course, it has grown due to inflation and our “successes” in the global economy... But all sorts of reports on pension decisions do not allow us to relax and wait for manna from heaven... And all these calculations with our government’s food “baskets” are just a waste of time laughter. Or slippers. And who gives THIS to the president to sign and what is he thinking about when signing the next “basket” of no more than 5,000 rubles a month - this is just something from the realm of fantasy, but you have to live on it. That is, by the time of retirement age, our employee is simply obliged to have iron health and an irresistible desire to continue working until his grave, provided that he is not asked to leave in an amicable way... Life, it tells him what to do, dictates, so to speak. And the prices for medicines simply whisper affectionately: “Work or lose money.”

And finally, I may be asked a question: why don’t you do this, man, or haven’t done it? The answer is: unfortunately, I learned about this system too late and at my age now it is useless to do this. I won't have time to save anything. And I would definitely do this. But for young people who are just entering life and working age and do not want any shocks and struggles in the form of revolutions and all sorts of cataclysms, perhaps such a model of survival as I have drawn here is quite suitable for a measured life. But you just need to start doing this at a young age. And our government is vague on this, but it insists. Otherwise, when retirement age comes, it will be very sad, and it seems that you only need to rely on yourself. In any case, this is what I always count on. There don’t seem to be any other options...

From January 1, 2015, pensions will be calculated according to new rules. Their final version It is currently in the discussion stage. But why was it necessary to change the previous procedure for calculating pensions?

According to the formula in force today, a person’s work experience practically does not affect the size of his pension, says State Secretary - Deputy Minister of Labor and Social Protection Andrei Pudov. - And this is unfair.

However, the point here is not even about justice and other moral criteria. The pension fund is replenished from insurance contributions paid by employers for their employees. The more people work, the more money is in the accounts from which pensions are paid to those who can no longer work. And we have more and more of them. Accordingly, a person with extensive experience is economically beneficial to the state. These people need to be encouraged and stimulated.

In the new pension formula, the stimulating effect is included in the insurance part of the labor pension. According to the official wording, it is calculated based on the sum of the coefficients of the insured person’s personal participation in the system. To put it simply, the amount of the insurance part of the pension directly depends on salary and length of service. It should be remembered that military service and child care are also included in the length of service.

According to the new rules, the minimum length of service required to receive a pension is planned to increase from five to fifteen years. This increase will occur gradually and smoothly until 2025.

Those who have less than 15 years of work experience are not entitled to an old-age pension. They can apply to the Pension Fund for a social pension, the size of which is smaller. True, this can only be done at the age of 60 for women and at 65 for men.

For everyone else, the retirement age will remain unchanged, explains the Minister of Labor and Social Protection of the Russian Federation Maxim Topilin. - That is, 60 years for men and 55 years for women.

Moreover, the later a person applies for an old-age labor pension after reaching this age, the higher the amount of his pension will be. It will be profitable to retire later. As Maxim Topilin put it, this is a chance for the middle class to get a normal pension.

But, in addition to length of service, other factors will determine the size of the pension. For example, the amount of salary. The higher it is, the higher the pension will be. The main thing is to remember that only the official, white salary is taken into account. The one with which the employer pays for the employee insurance premiums into the compulsory pension insurance system. In the case of a gray salary - the one in envelopes - no contributions are paid. Consequently, the pension is not formed and does not count toward the length of service.

You can now see how your pension will change depending on your salary and length of service and what you need to change in your life in order to receive more in old age using a special program. The so-called pension calculator works in 2013 prices according to the current formula and new formula. As they say, do the math and think about how to continue living. You can find this calculator on the websites: www. rosmintrud.ru and www.pfrf.ru.

The state takes care of each of its citizens, both in youth and especially in old age. When a person reaches retirement age and loses his ability to work, he goes to the state and receives a monthly pension - cash benefit established size. The average pension in Russia at the end of 2013 is 10,400 rubles. Living on such a benefit is not so easy; pensioners have to deny themselves a lot, and therefore they quickly become one of the most vulnerable segments of the population. Is there any way I can increase my pension?

How is the pension amount determined?

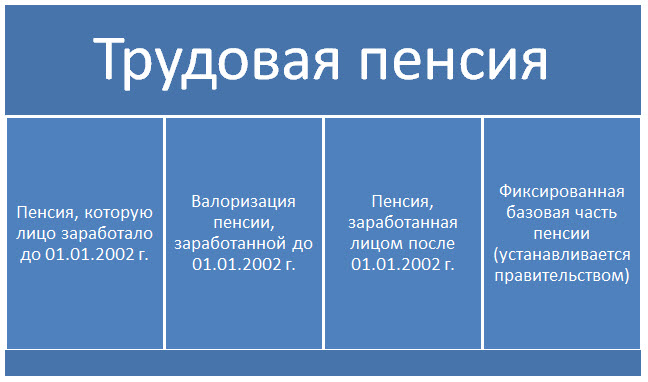

In order to be able to predict the amount of pension due to a person, you need to have an idea of how it is calculated. Currently, the labor pension consists of the insurance part and the funded part:

This is the formula for calculating the monthly pension for persons born after 1967 (for citizens born before 1967, the labor pension consists only of the insurance part). The insurance part of the pension can be calculated as follows:

SCh = PC / T + B, Where

SCH - insurance part of pension;

PC - pension capital accumulated by the employee in the form of deductions from wages throughout his entire working life;

T - number of months during which the person will receive a pension (the so-called survival period). This period is set by the government and is equal to 240 months (or 20 years);

B - the established basic amount of the insurance part of the labor pension, which is added to all pensioners without exception, and in 2014 it amounts to 3,610.31 rubles. This part of the pension is indexed annually taking into account the level of inflation, and can also increase if the person is disabled or lives in the north of the country.

Pension capital - sum Money, which the employee transferred to the Pension Fund for his entire career. There is a special formula for calculating pension capital:

PC = PC1 + SV + PC2, Where

PC1 - estimated pension capital, which was accumulated before 01/01/2002;

SV - amount of valorization- revaluation of the monetary value of pension rights acquired by the insured person before 01/01/2002. It is equal to 10% of PC1, and plus 1% to it for each full year of work experience before 01/01/1991;

PC2 - part of the pension capital that was formed after 01/01/2002. This part is recorded on the personal account of each employee, and therefore does not need to be calculated. Every year, each insured person receives letters from the Pension Fund, which indicate the amount of pension transfers to the person’s individual account.

Thus, general formula The calculation of the labor pension can be presented as follows:

Consequently, the size of the pension depends only on the amount of earnings that the insured person received during his life. The higher the salary, the greater the contributions to the employee’s individual pension account - the higher his pension as a result. Therefore, the government is agitating the population against salaries “in envelopes”. This is primarily in the interests of the citizens themselves - to receive a decent official wages. However, there are now many ways to increase your retirement savings.

Non-state pension funds

One of the ways to increase pension savings is to invest them in Non-state pension funds, which are management companies that manage pension savings of citizens in order to increase them. That is, citizens voluntarily transfer the funded part of their pension to NPFs, and they, by placing funds in assets, pay certain interest, thereby increasing the total amount of savings. On the one hand, such use of part of the pension is more profitable than simply accumulating it in the Pension Fund; and on the other hand, the person cannot see the real benefit, much less feel it in his wallet.

State co-financing of pensions

The state actively encourages its citizens to participate in co-financing their pension, that is, to invest additional funds into the account of the funded part of the pension. Moreover, as an incentive, the state will double the amount contributed by 2 times, but not more than 12,000 rubles. per year (if a person contributed 3,000 rubles, then the state will add another 3,000 rubles; but if a citizen adds 15,000 rubles per year to his savings, then the state will increase them by only 12,000 rubles). From the point of view of the benefits of the insured persons, such a program is dubious; it is much more profitable for people to accumulate money in other management companies at higher interest rates.

Sberbank pension savings

One of the most famous and largest banks in Russia offers its clients services for managing pension savings, or for opening “Pension” deposits with special conditions. The Security Council of the Russian Federation invites pensioners to open a deposit with interest capitalization, for a period of 1 year, with the possibility of unlimited replenishment and withdrawal of funds. There is one BUT: the interest on such deposits is scanty, the annual interest is only 3.5%. This level of income on a deposit is not able to cover even the current level of inflation in the country, and therefore such deposits can initially be considered unprofitable; By investing your pension in this way, you will not increase it, but will only lose part of the amount in the end.

Management companies and pensioners

Capital Financial Corporation Management Company can offer pensioners the placement of funds on favorable terms. If a person has a sufficiently large amount of money, then for this category of citizens there are deposits “” and “” - up to 17% annual return! The client has the right to choose the terms of the deposit - with capitalization or a one-time accrual of interest. By investing money in SFK Management Company, pensioners will be able to have additional income in the form of guaranteed interest on deposits!