Deductions to the pension fund from salary. Payroll taxes: everything everyone needs to know

At the accountant's office when calculating wages, calculation of taxes from salaries, calculation of insurance premiums and deductions of taxes from salaries to the budget, quite a lot of questions often arise. How to correctly calculate payroll taxes and accurately and timely make payroll tax deductions will be discussed in this article.

According to the legislation of the Russian Federation, income individuals subject to taxes and insurance contributions.

It is also important to correctly calculate wages and taxes, calculate personal income tax from wages and calculate insurance contributions that guarantee the employee social benefits, including payment sick leave, benefits and pensions.

How to calculate personal income tax on wages?

According to the provisions of the Tax Code of the Russian Federation, namely Articles 208 and 210: employee income received from sources in the Russian Federation is subject to personal income tax. Moreover, income tax is calculated on wages regardless of its size (see, for example, Letter of the Federal Tax Service of Russia for Moscow dated September 24, 2009 N 20-14/3/099660@).In order to calculate, withhold and transfer income tax from wages to the budget, an accountant needs to perform a number of actions, namely:

1. Determine the amount of taxable income and the tax base;

2. Determine the tax rate applicable to to this employee and to given income;

3. Calculate the amount of personal income tax;

4. Withhold the amount of tax from salary;

5. Calculate insurance premiums, including contributions to Pension Fund RF;

6. Transfer tax and insurance contributions to the budget.

But before you start calculating personal income tax on an employee’s salary, you need to determine his tax status. This is due to the fact that for persons who are not tax residents of the Russian Federation, the procedure for calculating tax will be different (clause 3 of Article 210, clause 3 of Article 224, clause 3 of Article 226 of the Tax Code of the Russian Federation).

To calculate personal income tax on wages, an employee’s income must be summed up on an accrual basis from the beginning of the year (clause 3 of Article 226 of the Tax Code of the Russian Federation). The amount of income includes wages accrued for the calculated period (clause 6, clause 1, article 208, clauses 2, 3, article 226 of the Tax Code of the Russian Federation).

It is important to take into account that payments in the form of financial assistance, as well as bonuses and incentives are included in the income of the month in which they are actually paid (clause 1 of Article 223 of the Tax Code of the Russian Federation) (see Letter of the Ministry of Finance of Russia dated November 12, 2007 N 03-04 -06-01/383).

When calculating the amount of taxable income, it is necessary to exclude all types of established current legislation compensation payments (within the amounts established by law) related to the employee’s performance of labor duties, which are not subject to personal income tax (clause 3 of article 217 of the Tax Code of the Russian Federation). For example: compensation for the use of personal vehicles for business purposes, compensation for work with special working conditions, compensation for the traveling nature of work, and others. Also, in order to calculate the salary tax, when determining taxable income, the amounts of deductions provided to the employee (standard, social, property, professional) are excluded.

The personal income tax rate is established by the Tax Code of the Russian Federation and is valid throughout Russia. Article 224 of the Tax Code of the Russian Federation sets personal income tax rates at 9%, 13%, 30% and 35%, depending on the type of income and tax status of the employee.

How to calculate payroll taxes - example:

The company Romashka LLC employs Semenov Ivan Petrovich, born in 1983, who is a tax resident, his salary is 10,000 rubles. per month, has one child 5 years old, was not on vacation or sick leave in 2014. Also Semenov I.P. owns 1% shares authorized capital in Romashka LLC and in January for 2013 received dividends in the amount of 15,000 rubles.From the table above it is clear that Semenov I.P. for January 2014, he received income in the amount of 22,532 rubles, and the Romashka LLC company, in compliance with the requirements of the legislation of the Russian Federation, calculated and withheld tax from the employee’s wages of 2,468 rubles.

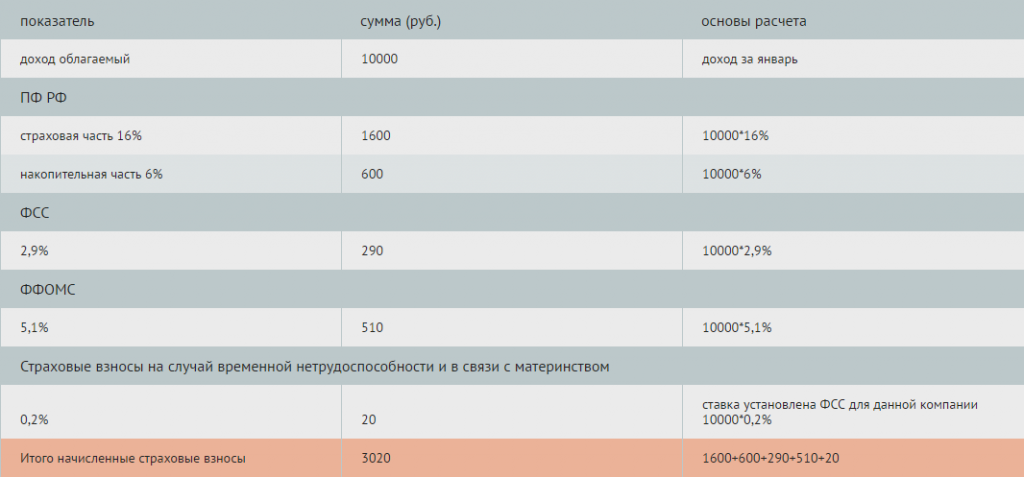

How to calculate insurance premiums from income - example:

Now we will calculate insurance premiums from the income of Semenov I.P.According to Art. 8 Federal Law No. 212-FZ dated July 24, 2009: the base for calculating insurance premiums for insurance premium payers is defined as the amount of payments and other remunerations provided for in Part 1 of Article 7 of Federal Law No. 212-FZ, accrued by insurance premium payers for the billing period in for the benefit of individuals, with the exception of the amounts specified in Article 9 of Federal Law No. 212-FZ.

Deductions from wages in the form of insurance contributions are provided for by the legislation of the Russian Federation. Also, to determine the size of insurance premiums, it is necessary to determine the type of income of the employee, his status, and know his date of birth.

We will calculate insurance contributions to the pension fund, social insurance fund, compulsory health insurance, insurance premiums in case of temporary disability and in connection with maternity.

Romashka LLC transferred the amount of personal income tax calculated and withheld to the budget of the Russian Federation.

Deduction of taxes from wages to the budget (NDFL) must be made directly when paying income to an employee, i.e. on the same day.

Insurance premiums are deducted from wages by insurance premium payers, separately to each state extra-budgetary fund.

During the billing period, the company pays insurance premiums in the form of monthly mandatory payments. The monthly obligatory payment is due no later than the 15th day of the calendar month following the calendar month for which the monthly obligatory payment is calculated.

The Intercomp company specializes in and taxes on it. Highly qualified specialists will give advice and assist in calculation and payment income tax from wages, calculation of insurance premiums, and will also promptly remind you of the need to pay taxes and submit reports on wages, taxes and insurance premiums

To maintain a successful financial activities state, citizens of a given state pay various contributions in its favor. The lion's share of these contributions comes from various taxes.

Due to recent changes in tax laws, many workers have become concerned about what kind of payroll tax they pay.

So, what taxes are paid on wages?

The main one is income tax or personal income tax (NDFL). This is 13% of your total income minus documented expenses.

There are types of income where the personal income tax rate increases, for example, if you win more than 4,000 rubles in the lottery. it will be 35% (won 5,000 rubles - received 3,250), or decreases, for example, if income from dividends is received, it will be 9%.

This tax is paid by the employee from accrued wages. However, this is not all.

What other taxes are payable on salary?

Also, based on the employee’s salary, the employer pays the following contributions to the budget:

- to the Pension Fund (the so-called compulsory insurance). The contribution is 26% of the salary.

- to the Social Insurance Fund is 2.9% of salary.

- Depending on the type of activity, a contribution is also made to the Social Insurance Fund for insurance against industrial accidents and occupational diseases. It all depends on the so-called occupational risk class. The Classification of Occupational Risk Classes, approved by Order of the Ministry of Health and Social Development of Russia No. 857, will help determine which category the payer belongs to (see Classifications of types of economic activities by occupational risk classes). The contribution can be from 0.2% of salary and higher.

- to the Federal Health Insurance Fund, contribution of 3.1%.

- to the Territorial Health Insurance Fund is 2%.

Thus, neither more nor less, the employer pays (or at least should) about 34% + 13% income tax based on our salary.

It is believed that these amounts go to the state budget to maintain its normal existence - maintaining government structures, hospitals, schools, maintaining security, etc.

What salary is not taxed?

The question is not entirely correct. IN in this case We're talking more about income. The list of income that is not subject to income taxes is quite long. This is for example:

- State benefits (eg, maternity benefits, unemployment);

- Pensions;

- Alimony;

- Scholarships;

- Rewards for donated blood;

- Income from collecting and selling berries, mushrooms, plants;

- Income of amateur hunters, etc., etc.

Salary is the remuneration of employees for work in a particular organization. Its size often depends on the complexity of the work, the qualifications of the worker himself and many other factors.

However, not everyone knows that employees receive slightly smaller amounts compared to their actual earnings. The reason for this is the withholding of taxes from salaries.

What it is?

Almost any type of income should be taxable. This provision also applies to wages, from which several types of contributions are deducted.

Thus, amounts intended to pay for three types of insurance are subject to deductions:

- social;

- medical;

- pension.

In 2017, these contributions are mandatory and must be paid to the tax authority, which is often confused with the Federal Migration Service.

In addition to these deductions, income tax is also calculated from a citizen’s salary.

The legislative framework

You can find out how much taxes are charged on wages from the legislation.

The main document in this case is the Labor Code of the Russian Federation. Also, accruals to the Pension Fund of the Russian Federation have their own scheme and are deducted in accordance with Article 10 of Federal Law No. 196.

Salary taxes

Taxes deducted from wages must be paid by the head of the organization or by the employee himself.

Some of them have strictly defined amounts, while others directly depend on the citizen’s earnings.

How much interest is deducted?

The amount of insurance payments changes every year, so it is quite difficult to say a specific amount. But among the deductions, the firmest position in terms of percentage occupies personal income tax.

According to the law, a citizen is obliged to allocate 13% of his earnings.

Many employers make these deductions for personal income tax even before transferring earnings to their employees. However, in the case of “black” salaries, these manipulations are not performed.

Therefore, the employee must independently declare his earnings to avoid penalties for tax evasion.

Income

The main tax on wages and other types of income is personal income tax. It is the income tax, as mentioned above, that directly depends on the citizen’s earnings and is 13%.

Unlike other payments, this type of tax is levied on almost any type of earnings.

At the same time, it is worth pointing out that personal income tax is 13% in relation to not all income. So, for example, its size can increase up to 35%.

If there is a child

If an employee has a child who is under 18 years old, then he can apply for deductions from tax deductions.

So, a parent can receive a deduction of 400 or 600 rubles for each of their minor children. The exact figure depends on whether the child is natural or adopted.

Also, the amount of deductions from contributions can be doubled. Such developments may arise as a result of the child being recognized as disabled. In addition, this increase in deductions is intended for single parents or guardians.

Other deductions

As already indicated, in addition to the basic income tax, other types of deductions can also be made from salaries.

Thus, amounts intended for several types of insurance are deducted from salaries. It is difficult to indicate their exact sizes, since they change every year depending on the economic situation of the state and other factors.

How can I reduce it?

Any manager wants to reduce the amounts that are withheld from the salaries of his subordinates. However, tax evasion methods are quite often illegal.

Thus, the most popular of the “illegal” methods is the payment of so-called “black” and “gray” salaries.

If an employee receives one or another type of income, then his earnings become slightly higher. But this happens only due to savings on insurance. In addition, if the employer is caught carrying out such a payment scheme, then not only he, but also some of the employees may be held liable.

But there are safer, legal methods. They also allow you to reduce the number of taxes. But it is worth considering that when using them, the company may attract closer attention from the tax authorities.

Thus, some employers, in order to avoid a number of payments, try to transfer wages to employees in the form of dividends. But this scheme is not always suitable.

To implement it, the company must be large enough; in addition, not all employees can receive such income.

There are also cases where employees receive earnings in the form of compensation. In this case, the employer intends to overstate the amount of compensation in local documents, and then delays wages. As a result, employees are paid the standard amount of earnings, but with smaller tax deductions.

But there are also less dangerous types of schemes in which a reduction in deductions is made through standard tax deductions.

One example of such deductions has already been given above, and was associated with the presence of a child. If an employee is officially employed, he can receive a professional deduction.

In addition to reducing personal income tax on wages, a working citizen can also reduce other types of taxes. For example, he can take advantage of a property deduction.

The size of legal deductions can vary from 400 rubles to 3 thousand rubles. The lowest amount of deductions can be received by employees whose official earnings do not exceed 20 thousand from the beginning of the year.

A larger amount of 500 rubles is deducted only if the employee was recognized as a hero of Russia or the USSR, or if he received any other awards.

The highest amounts of payments are awarded to mothers of many children, war veterans, and those recognized as victims of the Chernobyl disaster. It is worth noting that all deductions are made only from personal income tax. In addition, if an employee has two jobs, then a reduction in income tax is possible only from the basic earnings.

Is the premium taxable?

Income tax or personal income tax applies to almost all types of income, and bonuses are no exception.

As with earnings, personal income tax in the form of 13% is also deducted from them. The same rule applies to other allowances. However, insurance premiums are not collected from such payments.

Employer's liability

If an employer deliberately evades paying taxes and other deductions from the salaries of its employees, it must be aware of all the existing risks that can actually be encountered.

Thus, when “gray” or “black” schemes are identified, the legislation provides for punishment for the manager in the form of administrative liability.

According to the Tax Code of the Russian Federation, punishment can be expressed in penalties of up to 10%. The company will also be charged an additional amount equal to 20% of all unpaid taxes.

But in situations where the total amount of debt is large, the employer falls under criminal liability. In this case, regulation is carried out by Article 199 of the Criminal Code of the Russian Federation. IN best case scenario the manager will be fined up to 300 thousand, and in the worst case - arrest or complete imprisonment.

Video about paying taxes

The issue of reducing the tax burden is not urgent for accountants. This is due to the abolition of the single social tax for individual entrepreneurs and organizations with a simplified taxation system and its replacement with extra-budgetary funds, which make up 30% of the payroll in 2017. At the same time, the tax on personal income continues to exist. All this leads to a constant search for schemes to optimize remuneration, and as a consequence to a reduction in the tax burden.

You can reduce your salary fund in several ways:

Transfer payments to the “envelope” system;

Change the remuneration system by transferring it to a form other than the monetary equivalent;

Redistribution of basic wages into other forms.

Payroll calculation in 2017

In order to understand why to reduce the payroll, we will give an example of calculating insurance premiums. Suppose an employee receives a salary of 50,000 rubles. 13% is deducted from this amount (personal income tax), so in order to maintain the net salary at the level of 50 thousand, it is necessary to accrue 57,470 rubles. From this amount it is necessary to pay an insurance premium of 30% - 57470 * 30% = 17240 rubles. It will be possible to deduct only 20% of the amount spent from the enterprise: (50000+17240) * 20% = 13450 rubles.

Having paid income tax (6,500 rubles) and insurance premium (17,240 rubles), the company spent 23,740 rubles. for these payments. At the same time, I saved 13,450 rubles. on return. The net tax burden was 23,740 – 13,450 = 10,290 rubles. The relative one will be: 10290/50000 = 0.206 or 20.6%. With the simplified tax system it varies from 27 to 49.5%.

Thus, when calculating the relative burden, it is necessary to take into account: income tax (20%), personal income tax (13%), tax at 6% on income or 15% on the “income minus expenses” base, insurance premiums (30%). So, in order to pay the employee the stated salary, the company must increase the wage fund from 20 to 50%. Naturally, with such indicators, measures are necessary to reduce payroll costs.

Wage- the main income of the vast majority of individuals. And tax revenues are the main income for the state budget. Therefore, these two concepts are closely related in the economy of any country. So Russia has its own tax system, and regardless of the tax regime of the organization in which a person works, wages are calculated in the same way.

Remuneration for labor on the territory of the Russian Federation is made in a single national currency - rubles. Not cash payments, cannot exceed 20% of the total salary per month. The labor legislation of the Russian Federation clearly states the amount of the minimum wage (minimum wage). It turns out that the salary of an employee who has worked the standard hours for a month and regularly fulfills his duties prescribed in employment contract, should be higher than the minimum wage. The amount of wages must be agreed upon in advance between the employer and employee. And additional bonus systems, as a rule, are prescribed separately in internal regulations. Wages must be paid at least twice a month.

Taxes can be roughly divided into those paid by the employer, that is, those that do not affect the employee’s final salary, and taxes deducted from the final salary.

Payroll taxes paid by the employer:

Payroll taxes paid by the employee:

Now let's look at each one in order salary tax:

Payments to the Pension Fund. Payments within the framework of mandatory pension insurance- these are the largest contributions that the employer is required to make for each employee. The amount of contribution to the Pension Fund is 22% of wages.

Contributions to the fund social insurance. Also mandatory type insurance intended for cases of temporary disability or maternity. Deductions are equal to 2.9% of wages. The deduction rate may vary depending on the harmfulness of production.

Contributions to health insurance funds. Contrary to popular belief, medicine in our country is not free. Most services are paid from the balance of medical funds. And employers make contributions to these funds in the amount of 5.1% of wages.

Income tax . Every tax resident Russian Federation, is obliged to pay tax on his income. Therefore, every month the employer withholds 13% of personal income tax from the employee’s salary, freeing the latter from the need to fill out declarations and calculate taxes on his own. This is the only tax deducted directly from the final salary amount and paid by the employee. The percentage of personal income tax deductions depends on the type of income. But in the case of wages, it is a stable 13%. But in three specific cases it is possible to use tax deductions for salaries:

Deductions for disabled people since childhood (500 rubles tax deduction)

Deductions for each child under 18 years of age (1,400 rubles for each child)

Deductions for persons who eliminated the consequences of the accident at the Chernobyl nuclear power plant, for caring for a disabled child of groups 1 and 2 and others provided for by law (3,000 rubles).

To receive these deductions, you must document your right to use them and have a salary of less than 280,000 per month.

How to calculate the amount of personal income tax from wages.

As an example, let's take the most simple situation. Your employer has calculated your salary at 10,000 rubles. From this amount, we accordingly subtract 13% of income tax: 10,000 (wages) - 13% (1,300 rubles) = 8,700 rubles. It turns out that from a salary of 10,000 rubles, the employee will receive 8,700.

In conclusion, of course, it should be noted that all taxes and deductions were introduced not just to make a profit for the state, but primarily to create comfortable living conditions for every citizen of the country.